Cryptocurrency taxes: A guide to tax rules for Bitcoin, Ethereum and more

7 things you need to know about cryptocurrency taxes

With the astonishing expansion in the worth of some cryptographic forms of money like Bitcoin and Ethereum, crypto dealers and aficionados might experience genuine duty issues. The Internal Revenue Service (IRS) is moving forward implementation, and surprisingly the individuals who own cash—also exchanges—need to ensure they didn’t disregard the law. Given the manner in which the IRS handles cryptographic money, this might be more straightforward than you might suspect.

The individuals who use cryptographic money for exchanges have more motivation to comprehend the law and what burdens their activities will bring about. The uplifting news: The IRS treats digital currencies the same way it treats other significant resources like stocks and bonds. The awful news: This treatment likewise makes it hard to really utilize digital money to buy labor and products.

1. You’ll be asked whether you owned or used cryptocurrency

Your 2021 assessment form should state whether you use cryptographic money for exchanges. The 1040 structure in the clear at the top inquires: “Whenever in 2021, will you get, sell, send, trade, or in any case get any monetary advantages of any virtual cash?”

In this way, you will have the opportunity to answer clearly whether you use cryptocurrency for transactions, which gives you the opportunity to lie to the IRS. If you answer dishonestly, you may face further legal dangers, and the IRS will not sympathize with scammers and tax fraudsters.

2. You don’t escape being taxed just because you didn’t get a 1099

You (and the IRS) will normally get a 1099 structure from the bank or business firm that shows the pay you got during the year. Be that as it may, this may not be the situation with cryptographic forms of money.

Nonetheless, the law passed in November 2021 will require more definite duty reports for individuals in this industry from January 1, 2023. The law requires merchants remembering any individual who moves computerized resources for others for debate to report this data to the IRS upon demand 1099. or then again comparative structure.

3. Just using crypto exposes you to potential tax liability

Each time you convert virtual cash into genuine money, labor and products, you can make an assessment responsibility. In case the value you sell for your cryptographic money the worth of the product or the genuine cash you get surpasses your benchmark esteem in the digital currency, you will make a guarantee. Consequently, on the off chance that the worth you get surpasses the benefit of putting resources into digital money, you will be burdened.

Obviously, if the worth of products, administrations or genuine money is lower than the worth of your digital currency, you may likewise cause charge misfortunes. Regardless, to work out, you want to know your expense premise.

Kindly note that this isn’t an exchange charge. This is a capital increases charge an assessment on acknowledged changes in the worth of digital currencies. What’s more, actually like the stocks you purchase and hold, in case you don’t exchange digital currencies for different things, you will not create a gain or lose cash.

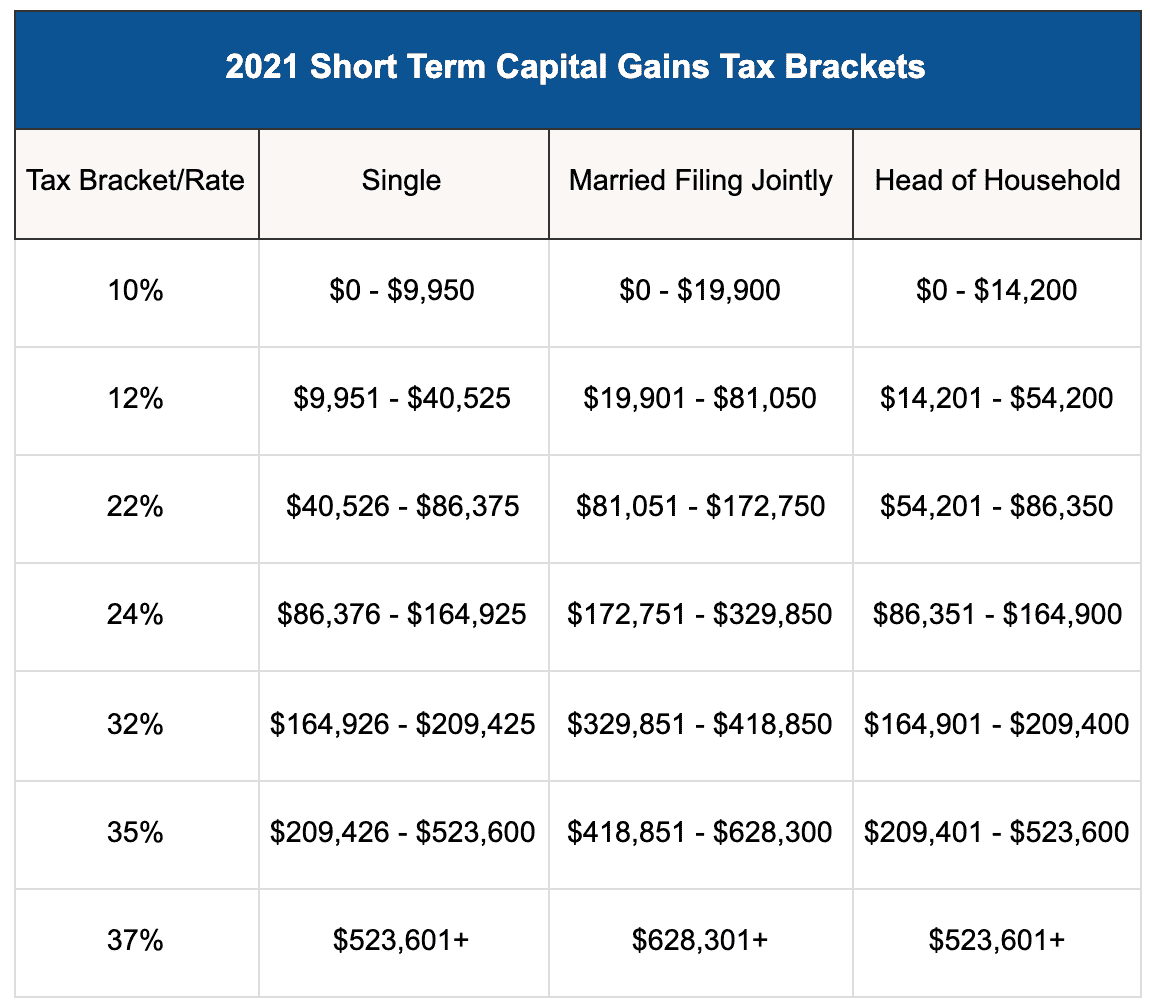

4. Gains on crypto trading are treated like regular capital gains

Things being what they are, would you say you are benefitting from an enormous number of exchanges or buys? The IRS for the most part treats cryptographic money gains similarly as a capital increases. As such, you will pay the typical transient capital additions charge rate for resources held for short of what one year (up to 37% in 2021 and 2022, contingent upon your pay). Yet, for resources held for over one year, over the long haul, you will make good on capital additions charge, which might be lower (0%, 15%, and 20%).

Similar standards for counterbalancing capital increases and misfortunes apply to cryptographic forms of money. Thusly, you can deduct capital misfortunes, with an overal deficit of up to $3,000 each year. In the event that your total deficit surpasses this sum, you should convey it forward to the following year.

5. Crypto miners may be treated differently from others

Do you consider cryptocurrency as a business? Then you can deduct your expenses like in regular business. Your income is the value of the products you produce.

But the last point is crucial: you must be engaged in trade or business to qualify. You cannot use your mining equipment as a hobby and get the same deduction as your actual business.

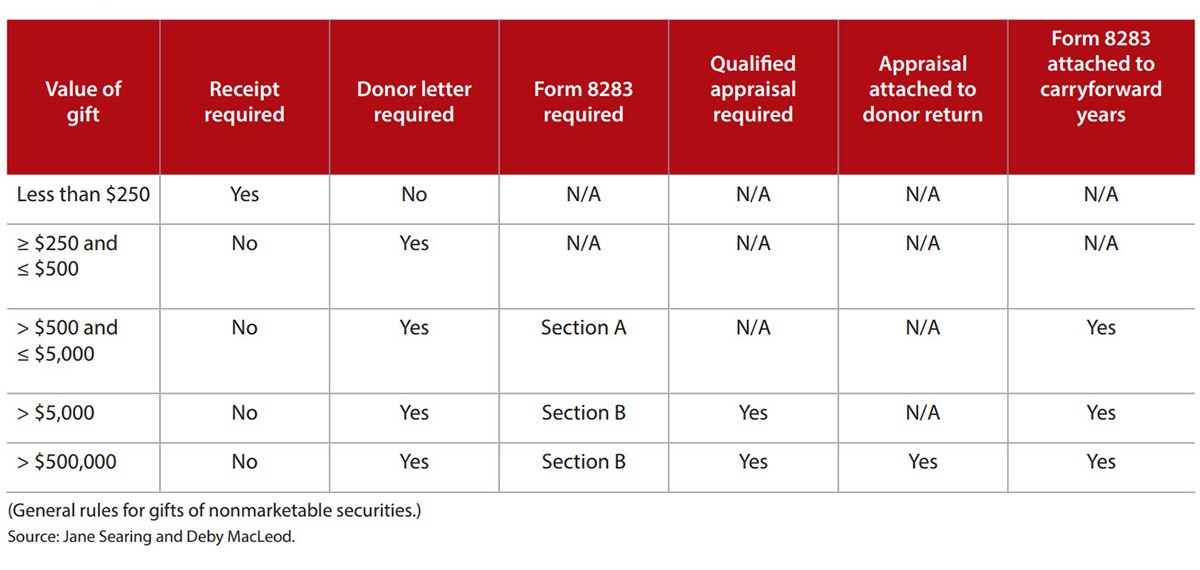

6. A gift of crypto is treated the same as other gifts

In the event that you give cryptographic money to somebody, potentially a youthful comparative with keep your premium, your gift will be dealt with like some other comparable gift. Subsequently, on the off chance that it surpasses $15,000 in 2021 (or $16,000 in 2022), it very well might be likely to gift charge. Assuming that it is the ideal opportunity for the beneficiary to sell the gift, the expense base and the contributor cost base stay unaltered.

Nonetheless, regardless of whether you surpass the yearly edge, there are multiple ways of keeping away from gift charge, for example, exploiting a lifetime charge exception.

7. Inherited cryptocurrency is treated like other inherited assets

Conventional cryptographic forms of money are viewed as other fixed resources and can be given from one age to another. Assuming the property surpasses specific edges (US$11.7 million and US$12.06 million of every 2021 and 2022, separately), they might be needed to make good on legacy charges. Like stocks, the reasonable worth of digital forms of money has ascended upon the arrival of their passing. Accordingly, for a great many people, digital currency is viewed as a regular capital resource.

The real utilization of cryptographic money can be shockingly awkward, beginning with following your expense base, posting your powerful selling cost, and afterward conceivably covering charges (regardless of whether there is no formal 1099 assertion). Likewise, the U.S. Inward Revenue Service is moving forward its investigation and examination of likely tax avoidance via cautiously seeing who is trading cryptographic forms of money. This large number of elements make digital currency hard to utilize and may prevent its more extensive reception.